Fiscal woes, debt overhang but no crash

Economist sees a difficult transition, but thinks country will dodge bullet of financial crisis

Leading economist George Magnus believes China is set to face a severe fiscal squeeze. Fiscal revenues are set to grow at just 1 percent this year, the slowest growth since 1981, according to a Deutsche Bank report.

Such a fall in revenues could lead to China's debt position - already 250 percent of GDP by some estimates - worsening.

|

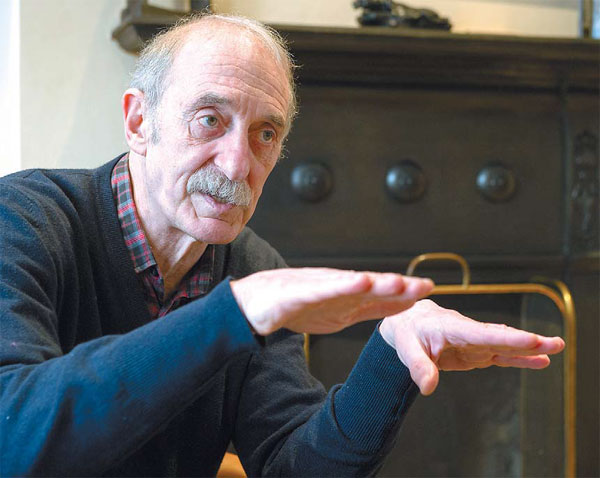

George Magnus, senior independent economist at the Swiss bank UBS, has predicted that China could face debt crisis this decade. Nick J. B. Moore / For China Daily |

"I think it is one of those difficult periods of transition that China is going through, principally because of the fallout and slowdown in real estate and also what is happening to land prices, which comprise about 25 to 30 percent of local government revenues," he says.

Magnus, senior independent economist at the Swiss bank UBS, says the problem is compounded by the fact a new source of local government funding, the issuance of bonds, is unlikely to be up and running for up to a year.

He estimates the decline in real estate prices combined with the lag before the introduction of bonds could lead to a 1.5 trillion yuan ($240 billion; 210 billion euros) loss of revenue, equivalent to 1.6 percent of GDP.

"One has to assume Beijing is aware of this and there will be some other coping mechanism to fill the gap but it is unquestionably a problem."

Magnus, 65, was speaking in the front room of his Edwardian house in Highgate, north London.

He was one of the few economists to predict the financial crisis some two years before the Lehman Brothers collapse in 2008.

As someone who is also a regular commentator on China, his views on the economy's debt position carry some authority.

In his 2010 book, Uprising: Will Emerging Markets Shape or Shake the World Economy?, which was translated into Chinese, he predicted China was likely to face some sort of debt crisis this decade.

"Well, we are five years into the decade. I suppose my views have changed a little bit in that the stasis that China seemed to have become sunk into has certainly been shocked by the new leadership," he says.

"It would be churlish to dismiss the anti-corruption campaign, which is about improving the efficiency of the whole government apparatus and optimizing the system, since it is obviously having an effect."

He believes despite slowing fiscal revenues and growing debt, China will probably avert a financial crisis.

"I just don't think there is any point in anticipating or trying to predict China is going to have a financial crisis because the likelihood is that it probably won't. It can probably internalize it in ways that we in the West can't. This does not mean, however, that it hasn't got a debt or a growth issue because it clearly has."

He says China's current problems stem from 2010 and are largely the result of the 4 trillion yuan stimulus package designed to ease the effects of the global financial crisis. This has led to a huge increase in the debt to GDP ratio from 170 to the current 250 percent.

"Of that increase, the lion's share is accounted for by local government and non-financial enterprises, largely China's state-owned enterprises."

Magnus says the strains on local government finances would be less of a problem if there were not at the same time knock-on effects from a slump in real estate spending.

"If this was the only thing happening we probably wouldn't be worried about it but it happens to be taking place in the context of a broadly based decline in real estate investment, which is spilling over to other investments, and so these things tend to feed on themselves."

He says this combination of factors is likely to impact on China's GDP growth for 2015. The government set a target of (about) 7 percent on March 5 but he believes the outcome will be short of that.

"I think it will be shy of 6.5 percent, at 6.4 or maybe 6.3 percent, which would be at the low end of expectations.

"For me it represents another station on the way to the terminus of a 4 to 4.5 percent growth rate. I don't think it is going to happen very quickly but will be a sequential process."

Magnus, who began his career as an economics writer with the UK civil service in the 1970s, has held a number of prominent economist roles with Lloyds Bank, Bank of America and SG Warburg, where he was chief economist.

He joined UBS in 1997 and was in turn its chief economist and senior economic adviser before formally leaving in 2012. He now has an independent role in the bank attending client-related functions and meetings.

He first visited China in the late 1990s but it was not until the middle of the last decade that he began to take a keen interest when he started to specialize in emerging markets for UBS.

"I had a loose interest until then. It was clearly an increasingly important country but not one I spent much of my professional time investigating. When I began to focus on emerging markets, it was clear that China to a large extent was the emerging markets by itself."

He is now somewhat disparaging about the hype that once surrounded emerging markets.

"I think acronyms such as BRICS (Brazil, Russia, India, China and South Africa) and MINT (Mexico, Indonesia, Nigeria and Turkey) are pretty much dead. The latter though has obviously gone wrong much quicker than BRICS," he says.

"They are clever marketing tools but now I don't see any reason why emerging countries should be seen as a part of some universal family. I think it is now very much horses for courses."

He says he is firmly of the view that the Chinese economy - despite current difficulties - is not going to suffer some collapse as predicted by US hedge fund billionaire Jim Chanos among others.

"There are some ardent diehards that say China is about to implode. I am not one of those who is forecasting China is going to have a Lehman's moment. You have actually had the problems in the real estate sector that Chanos predicted, and the economy is not collapsing. I think also that the debate about hard and soft landing has also pretty much dried up.

"Even in these indebted times, China's current level of debt is high compared to many developed countries. Developing countries like China are also said to find it more difficult to service their debt because they do not have the same stock of wealth.

"That is the theory, although in some cases this is clearly not true, particularly if you look at southern Europe. I think, however, that China as the second biggest economy in the world ought to be able to carry its debt burden because of its sheer size in ways that other countries that may be richer in term of income per head can't do."

One of the key questions about China - as with other emerging market economies - is whether it will get stuck in the so-called middle-income trap and never advance properly to being a fully developed nation.

"I really don't think you can judge that because China hasn't been a middle income country long enough to tell whether it has been trapped. You have to be there for 10 to 15 years to have the proof you can't get out."

The global backdrop is not good for any emerging economy at present, let alone China, with many warning of a global debt deflationary spiral.

"Because of the 50 percent drop in oil prices, I would say most economists should be feeling a little bit better about what lies ahead in 2015 simply because it presents an unexpected tailwind," he says.

As for China, Magnus believes many commentators find it difficult to understand its economy.

"Trying to look at China through Western eyes doesn't really work. People see it having a conventional financial and debt crisis. The economy is undergoing quite a lot of reform that was all outlined at the Third Plenum. We will have to work out over the space of the next decade what has worked and what remains needed to be done."

andrewmoody@chinadaily.com.cn