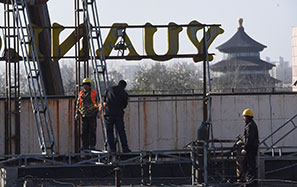

Default 'sign of stress' in property sector

The default of Zhejiang Xingrun Real Estate Co may portend difficult times ahead for small developers amid emerging risks in third- and fourth-tier cities, analysts said.

On Tuesday, several media reports said that Zhejiang Xingrun, a private property developer in Fenghua, Zhejiang province, is likely to default on 3.5 billion yuan ($573 million) in debt owed to several banks, as well as other obligations.

The Financial Times also reported that the People's Bank of China had held a meeting with the local government and other banks to discuss the case.

But the central bank has denied that any such meeting took place.

"We believe this is merely one example of many distressed small developers in China," said Bei Fu, credit analyst with Standard & Poor's Financial Services LLC, adding that most of these companies own only one or few projects.

Chen Li, chief China strategist at UBS Securities Co Ltd, said there will be further defaults in the real estate sector for a variety of reasons: oversupply in smaller cities, significantly slower growth rates and weaker profit margins.

But Chen said defaults will be limited to smaller companies such as Zhejiang Xingrun.

Periods of oversupply aren't that unusual, though such conditions strain profitability and liquidity as inventories are reduced. But larger developers can lower their risks by diversifying into multiple markets, underscoring the importance of scale, according to Bei.

"So far, listed property developers' cash flows remain healthy, thanks to robust sales last year. Moreover, they have better access to capital than smaller developers," said Chen.

Large developers can obtain construction funding from banks at 6 percent to 9 percent. But smaller ones pay up to 20 percent, and they also grapple with limited availability of funds and refinancing risks. Most of them have turned to trust financing as an alternative to bank borrowing.

Trust financing is a form of asset securitization used by several industries in China. When developers raise money in this way, they package projects and use them as collateral for a bank loan. Banks sell units of these financing packages to institutional investors.

According to the China Trustee Association, more than 10 percent of new trust loans in 2013 were extended to the property sector, and the majority of that went to small developers who didn't have other viable funding channels.

Zhang Zhiwei, China economist with Nomura Securities Co Ltd, said China's property sector has significant excess investment, especially in third- and fourth-tier cities, which accounted for 67 percent of housing under construction last year.

"This risk does not seem to be fully recognized in the market, partly because data are not readily available for these cities, and some investors may be misled by the boom in first-tier cities," said Zhang.

For example, the market in Ningbo shows signs of overbuilding. According to data from the China Real Estate Information Corp, Ningbo had salable inventory of 32 months as of Feb 28, compared with the average of about 15 months in 13 major cities CRIC tracks.

Moreover, the manner in which the Chinese authorities resolve these defaults will have important implications.

Song Huiyong, a research director at Shanghai Centaline Property Consultants, said that neither commercial banks nor the PBOC should be held accountable for a particular company's capital woes, especially as the government aims to let the market play a bigger role.

Song said Xingrun's capital shortfall was a special case reflecting poor management.

"We believe the authorities will force shareholders and some of the lenders, especially from outside the traditional sectors, to realize their losses," said Chang.

Local governments will likely find ways to complete and deliver the units under construction to avert challenges from buyers who have already paid for their units.

This may include providing incentives to stronger homebuilders to take over the troubled projects, Chang said.

Despite challenging operational and financing conditions, S&P said it expects most of the developers to be able to weather the current turmoil.

They're usually listed and have reasonably good bank relationships and capital market standing. Many have lowered their exposure to trust financing over the past two years, the ratings agency said.

Wang Ying contributed to this story.

huyuanyuan@chinadaily.com.cn